About the Wealth Management Client Experience ROI Study

Wealth management firms are struggling to differentiate themselves, as investment advisors find it increasingly difficult to outperform their benchmarks.

In an environment characterized by regulatory scrutiny, consumer distrust, and disruptive technology, how can wealth management companies succeed? For many, the answer has been to lower their management fees and effectively turn the business into a commodity.

We thought there might be a better answer, and that was the spark for our Wealth Management Client Experience ROI Study – where we sought to explore the impact of good and bad client experiences, using the universal business “language” of shareholder value.

What we discovered should be of keen interest to financial services professionals — because, as it turns out, in this industry that’s focused on building and maintaining wealth, the greatest riches go to those who deliver an excellent client experience.

Best regards,

Jon Picoult

Founder & Principal, Watermark Consulting

Author, From Impressed To Obsessed

(Follow me on LinkedIn and Instagram)

The Business Challenge

The wealth management industry is, for lack of a better term, under siege.

Over the past decade, this industry has had to grapple with new realities that have fundamentally changed the nature of the business and its competitive landscape:

- An erosion of trust. Consumer trust in financial services deteriorated during the Great Recession and has struggled to recover. According to the 2026 Edelman Trust Barometer, financial services is the second least trusted industry in consumers’ eyes (landing ahead of only social media firms).

- A spotlight on fees and conflicts. Regulators, as well as increasingly informed consumers, have focused attention on the industry’s transparency (or lack thereof) with regard to fees and conflicts of interest. Business practices that were common in the past are now under scrutiny.

- Skepticism about stock-picking. As actively managed funds increasingly underperformed their benchmarks, lower-priced passive investments have surged in popularity – leaving industry players wondering: if it’s not investment returns that will differentiate us, then what will?

- The rise of the AI robo-advisors. Low-cost, automated investment management solutions have garnered attention in the marketplace, putting greater pressure on financial professionals to defend their fees and demonstrate their value.

- A race to the bottom. Firms are challenged by how to differentiate themselves in this new environment. As a result, some have resorted to pure price competition (cutting fees as low as zero points), and this has only served to further commoditize the industry’s offerings.

To combat these headwinds, and shape consumer perceptions more positively, financial services firms spend tens of billions of dollars each year in advertising. However, as these companies will eventually discover, you can’t advertise your way to a great client experience. Ultimately, clients’ perceptions will be shaped by the end-to-end experience itself – from how they’re onboarded, to how their needs are assessed, to how they’re kept informed, to how their investment portfolio performs over time.

Nevertheless, many industry players cling to a product-centric, rather than client-centric, view of the world. As a result, they subject their clients to a variety of frustrations and annoyances: Poorly designed websites, complicated onboarding processes, unintelligible disclosures, confusing account statements, interminable waits for client service, infuriatingly unhelpful AI chatbots, and overall poor responsiveness. As a result, they miss key opportunities to forge lifelong brand loyalty.

There are exceptions, however. Some wealth management firms are more deliberate in how they shape the prospect-to-client experience. And, as you’ll see in a moment, that strategy is rewarded by consumers and investors alike.

First, though, an explanation of the thought process behind the Wealth Management Client Experience ROI Study:

Our objective with this analysis was to help wealth management industry leaders understand the overarching influence of a great client experience (as well as a poor one). To accomplish that, we sought to elevate the dialogue. That meant getting the industry to focus, at least for a moment, not on the cost/benefit of specific client experience initiatives, but rather, on the macro impact of an effective client experience strategy.

We accomplished this by studying the cumulative total stock returns for two model portfolios – comprised of the Top 4 (“Leaders”) and Bottom 4 (“Laggards”) publicly traded companies in J.D. Power and Associates’ annual Full-Service Investor Satisfaction Studies. (A full description of the study’s methodology is available at the bottom of this article, and we’ve also compiled a list of frequently asked questions about the analysis.)

As the graphic in the next section vividly illustrates, the results of the latest Wealth Management Client Experience ROI Study continue to be quite compelling.

Wealth Management CX ROI Study Results

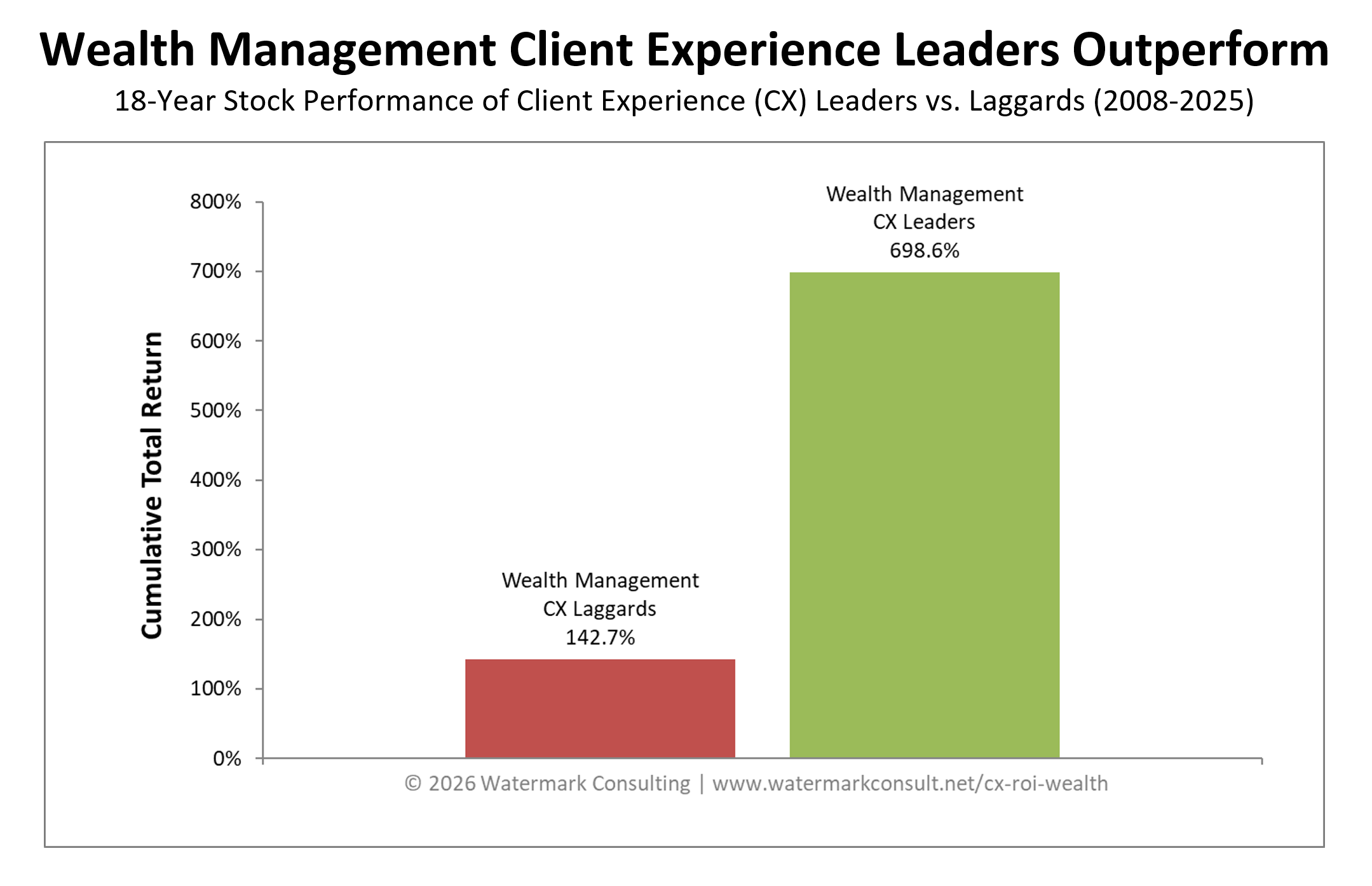

Our latest analysis incorporates 18 years of client experience rankings for wealth management firms. The graph below shows the cumulative total return across that period for the Client Experience Leaders and Laggards.

-

Wealth Management Client Experience Leaders far outperformed the Laggards, and the size of the performance differential (556 points) was striking.

-

Wealth Management Client Experience Leaders generated a total cumulative return that was 4.9 times greater than that of the Client Experience Laggards.

-

The performance gap between the Wealth Management CX Leaders & Laggards has more than tripled over the past five years.

Behind The Numbers

It’s worth underscoring that this analysis reflects nearly two decades of performance results, spanning entire economic cycles, from expansions to recessions. Over that period, the fortunes of Wealth Management Client Experience Leaders and Laggards have diverged in a dramatic and revealing way. What’s driving the disparity in performance across these two groups?

While there are obviously many factors that influence a company’s stock price, the results of this study indicate that, over the long-term, a great client experience helps build business value, while a poor client experience erodes it. That’s an important takeaway, for public and private entities alike.

But what exactly is creating that enhanced value? Answering that question requires understanding the economic calculus behind great client experiences. When a company consistently delivers an impressive experience to clients, it triggers behaviors that influence business financials in two important ways:

- A great CX helps grow revenues. When most people think about the economic benefit from a great client experience, this is where their heads go. And that’s entirely appropriate, because revenue growth is indeed one clear advantage of CX excellence. Why? Happy, loyal clients have better retention, they’re less price-sensitive and they’re more willing to entertain offers for other products and services – all helping to raise revenue. Plus, because they love you so much, they spread positive word-of-mouth and refer new clients to you – lifting revenue even higher.

- A great CX helps control (if not reduce) expenses. This is the part of the client experience economic equation that many businesses fail to appreciate. (It’s also why using revenue growth, alone, to demonstrate client experience ROI is misguided.) When you have happy, loyal clients, it has a very favorable influence on operating expenses. For example, due to all the client referrals you’re getting, you can spend less on new business acquisition – which reduces expenses. In addition, happy clients tend to complain less, putting reduced stress on your operating infrastructure (e.g., lower call and chat volumes), thereby also helping to keep expenses in check.

Higher revenues and a more competitive cost structure translate into superior profitability, and that’s what helps fuel exceptional shareholder returns for the CX Leaders.

Of course, those economic forces cut both ways. In contrast to the CX Leaders, the CX Laggards struggle to raise revenue (e.g., poor retention, high price-sensitivity, limited cross-purchasing, negative word-of-mouth) and they’re burdened with higher expenses (e.g., to acquire new clients, and to deal with the existing unhappy ones). This weighs on their long-term profitability and makes them less valuable in the eyes of the market.

Learn From The Leaders

How do Client Experience Leading firms create such positive, loyalty-enhancing impressions on the people they serve? It doesn’t happen by accident. They’re all essentially employing the same strategic approach to achieve that outcome — and it’s an approach that Watermark has documented through its “12 Principles” (a CX design framework that is more fully described in Watermark Founder Jon Picoult’s book From Impressed To Obsessed).

In addition to those CX design techniques, the CX Leaders also embrace a few fundamental, shared philosophies that help guide their efforts:

1. They aim for more than client satisfaction.

Satisfied clients defect all the time. And clients who are merely satisfied are far less likely to drive business growth through referrals, repeat purchases and reduced price sensitivity. Maximizing the return on CX investments requires more than just satisfying clients, it requires impressing them.

2. They leave nothing to chance.

The Leading companies have a keen appreciation for the wide array of live, print, and digital touchpoints that comprise their client experience. They design each of these touchpoints very intentionally, carefully choreographing the interaction to create an experience that consistently nails the basics and also delivers pleasant surprises.

3. They shape memories, not just experiences.

How people remember the client experience is arguably more important than the experience itself, as it’s those memories that ultimately drive repurchase and referral behavior. The Leading companies recognize this, and they use cognitive science to engineer experiences that people both enjoy in the moment and also remember fondly in the future.

4. They capitalize on the power of emotion.

People’s affinity toward a business is ultimately shaped by how they feel after interacting with the company, its representatives, and/or its products. CX-leading firms recognize this, and so they engineer experiences that don’t just focus on clients’ rational requirements, but also address their emotional needs.

5. They focus on both the client and the employee experience.

Happy, engaged employees help create happy, loyal clients (who, in turn, help create more happy, engaged employees). The value of this virtuous cycle cannot be overstated, and it’s why the most successful companies address both sides of this equation – obsessing not just over their clients, but also over the employees who serve them.

Implications For Wealth Management Firms

The results of this study suggest there is competitive advantage to be gained in the wealth management industry by differentiating along the client experience axis.

However, achieving that competitive differentiation requires that wealth management firms look at their business through a different lens, and embrace some unconventional operating principles – some examples of which we present below:

♦ Retention is not a good proxy for loyalty.

Wealth management firms often rely on account or asset retention to gauge the quality of their client experience. While retention is a valuable metric, it can be a misleading indicator of client perception (after all, a retained client may not necessarily be a loyal one).

As a result, many firms tend to overrate the quality of their client experience, and would benefit by complementing their internal performance gauges (e.g., client retention, asset growth) with more externally and behaviorally-focused measures (e.g., client referral frequency, Voice-of-the-Client feedback surveys, qualitative client research).

♦ Disclosure does not equal transparency.

The wealth management industry often points to its disclosure practices as evidence of its trustworthiness (i.e., “we’re not hiding anything from our clients, it’s all spelled out in our disclosures!”).

What the industry neglects to realize is that the manner by which information is disclosed is as consequential as the information itself.

Investment disclosures (regarding conflicts of interest, commissions, fees, etc.) are typically dense, difficult-to-read documents which leave the average consumer more confused than informed.

To earn client trust, financial services firms must strive for true transparency. That means eliminating the small print, skipping the legalese, and communicating with clients in clear, simple terms they can easily understand.

♦ Fiduciary is not a four-letter word.

When the U.S. government proposed rules that would have required more financial services professionals to act in their clients’ best interests, many in the industry were vocal in their opposition.

Adhering to that “fiduciary” standard, they argued, would be administratively onerous and costly (as compared to the “suitability” standard employed by many investment professionals). That the industry neglected to appreciate the consumer optics around this stance is a symptom of a much larger problem.

It’s difficult to deliver a great brand experience when people know (or eventually discover) that a business puts its interests ahead of the client’s. For this reason, financial professionals who serve as fiduciaries should wave that banner proudly.

As for the individuals and firms who resist that operating model, they should at least move beyond the industry’s traditional techniques of disclosure and clearly explain to those they serve (using plain language and real-life examples) the true nature and economics of the client relationship.

♦ Emotions are as critical as earnings.

Brokers and advisors who focus primarily on investment earnings are destined to deliver a mediocre client experience (or something worse).

The best and most memorable client experiences are those that strike an emotional chord in people – be it by accentuating positive feelings or mitigating negative ones. Many wealth and asset managers don’t fully appreciate this. As a result, they miss opportunities to enhance the client experience by, for example, celebrating clients’ planning milestones or addressing their sources of anxiety.

People might not remember the exact rate of return a financial advisor achieved, but they’ll surely remember how that advisor made them feel – confident or confused, assured or anxious, informed or ignorant. When it comes to building client loyalty, it’s those emotional responses that make all the difference.

Conclusion

One key accountability of financial services professionals is to help their clients manage risk. Ironically, though, many in this industry are failing to address a key risk that looms over their business.

It’s the risk that they become marginalized in an environment where their products and services are viewed as a commodity. It’s the risk that even the fundamental value of wealth management providers is called into question, as consumers become increasingly skeptical and distrustful of the industry.

However, there is a solution. The best way for wealth managers and financial planners to avoid the death spiral of commoditization is by delivering an exceptional end-to-end client experience – one that is devoid of common frustrations, one that inspires confidence, one that cultivates trust.

As this study has demonstrated, that’s the kind of client experience that is rewarded by both Main Street and Wall Street.

(Want more? Check out Watermark’s other Customer Experience ROI Studies here.)

Ready to Turn Your Organization into a CX Leader?

Watermark is a customer experience advisory firm that serves some of the world’s leading brands. We help companies impress their customers and inspire their employees, creating raving fans that drive business growth.

What’s your challenge?

- We need to make the case for CX at our company. Our executive education programs will help demonstrate the value of customer experience excellence to company leaders, and show them how time-tested CX design techniques could be applied to your business.

- We don’t really know what customers think of us. Our Consulting Services include quantitative and qualitative tools which help bring the voice of your customer to the forefront, revealing game-changing insights that will drive your business forward.

- We need to rally our employees around CX. Watermark founder Jon Picoult is an acclaimed keynote speaker. Invite Jon to your next all-employee meeting, sales conference or corporate event – he’ll inspire your team to deliver CX excellence, and show them exactly how to do it.

- We need to improve our CX, but we’re not sure where or how to start. Our Consulting Services, including Watermark’s proprietary “Customer Experience Reality Check” will evaluate your current CX and develop a detailed roadmap for turning it into a competitive differentiator.

Through our Customer Experience ROI Studies, we’ve uncovered the techniques that top companies use to turn everyday people into loyal brand advocates. Let us help you apply the same techniques to your business. Contact us to start the conversation.

Study Methodology

The Watermark Consulting Wealth Management Client Experience ROI Study is based on the cumulative total stock return for equally weighted, annually readjusted model portfolios comprised of Wealth Management Client Experience (CX) Leaders and Laggards.

For each year covered by the study, CX Leaders and CX Laggards were identified via J.D. Power and Associates’ annual Full-Service Investor Satisfaction Study. In any given year, the Leaders and Laggards were defined as the Top 4 and Bottom 4 publicly traded companies in these rankings (which generally represented the top and bottom quartiles of the ratings).

Portfolio returns were based on the prior-year performance of the Leaders and Laggards, to ensure that the results were not influenced by the publication of the research studies themselves.