About the Banking Customer Experience ROI Study

What’s a great customer experience really worth to a bank?

What’s a great customer experience really worth to a bank?

It’s a fair question in an industry that many would characterize as a commoditized business, where consumers often gravitate to the financial institution that offers the most competitive rates and lowest fees on their products.

However, we suspected that there were other experiential attributes (in addition to rates and fees) that helped shape consumers’ selection of a bank, as well as influence the word-of-mouth they spread to other potential customers.

So, we set out to determine if there really was a Customer Experience ROI, even in the seemingly commoditized business of retail banking. We sought to explore the impact of good and bad banking customer experiences, using the universal business “language” of shareholder value.

What we discovered should be of keen interest to banking professionals — because, as it turns out, in this industry that’s focused on managing money, the greatest riches go to those who deliver an excellent customer experience.

Best regards,

Jon Picoult

Founder & Principal, Watermark Consulting

Author, From Impressed To Obsessed

(Follow me on LinkedIn and Instagram)

The Business Challenge

In recent years, the retail banking industry has had to grapple with new realities that have fundamentally changed the nature of the business and its competitive landscape:

- An erosion of trust. Consumer trust in financial services deteriorated during the Great Recession and has struggled to recover. According to the 2026 Edelman Trust Barometer, financial services is the second least trusted industry in consumers’ eyes (landing ahead of only social media firms).

- A spotlight on fees. Financial regulators have intensified their focus on the fees banks charge, with the goal of improving transparency and eliminating excessive fees that are a common source of frustration for customers.

- More frictionless switching. With online tools, it’s become far easier for consumers to research other banks’ offerings and shift funds between institutions. Logistical barriers and switching costs that previously helped banks retain their deposits have now melted away.

- Competition from non-traditional players. Low-cost, AI-powered financial management solutions have garnered attention in the marketplace, making it more difficult for banks to position themselves as the go-to source for money management advice. Fintechs are also increasingly encroaching on banks’ traditional turf, such as home lending — business segments where banks previously encountered little competition.

To combat these headwinds, and shape consumer perceptions more favorably, the banking industry spends tens of billions of dollars each year in advertising.

However, as these financial institutions will eventually discover, you can’t advertise your way to a great customer experience. Ultimately, customers’ perceptions will be shaped by the end-to-end experience itself – from how they’re onboarded, to how their needs are assessed, to how they’re kept informed, to how effectively their banking products perform over time.

Nevertheless, many banks cling to a product-centric, rather than customer-centric, view of the world. To put it bluntly, this is an industry that is far more enamored with acquiring new customers than it is with delighting the ones they already have.

As a result, many banks subject their customers to a variety of frustrations and annoyances: Complex product portfolios, poorly explained product features, unintelligible disclosures, confusing account statements, interminable waits for customer service, infuriatingly unhelpful AI chatbots, clumsy digital account management tools, and overall poor responsiveness. As a result, they miss key opportunities to forge lifelong brand loyalty.

There are exceptions, however. Some banks are more deliberate in how they shape the prospect-to-customer experience. And, as you’ll see in a moment, that strategy is rewarded by consumers and investors alike.

First, though, an explanation of the thought process behind the Banking Customer Experience ROI Study:

Our objective with this analysis was to help banking industry leaders understand the overarching influence of a great customer experience (as well as a poor one). To accomplish that, we sought to elevate the dialogue. That meant getting the industry to focus, at least for a moment, not on the cost/benefit of specific customer experience initiatives, but rather, on the macro impact of an effective customer experience strategy.

We accomplished this by studying the cumulative total stock returns for two model portfolios – comprised of the Top 3 (“Leaders”) and Bottom 3 (“Laggards”) publicly traded companies in J.D. Power and Associates’ annual U.S. National Banking Satisfaction Studies. (A full description of the study’s methodology is available at the bottom of this article, and we’ve also compiled a list of frequently asked questions about the analysis.)

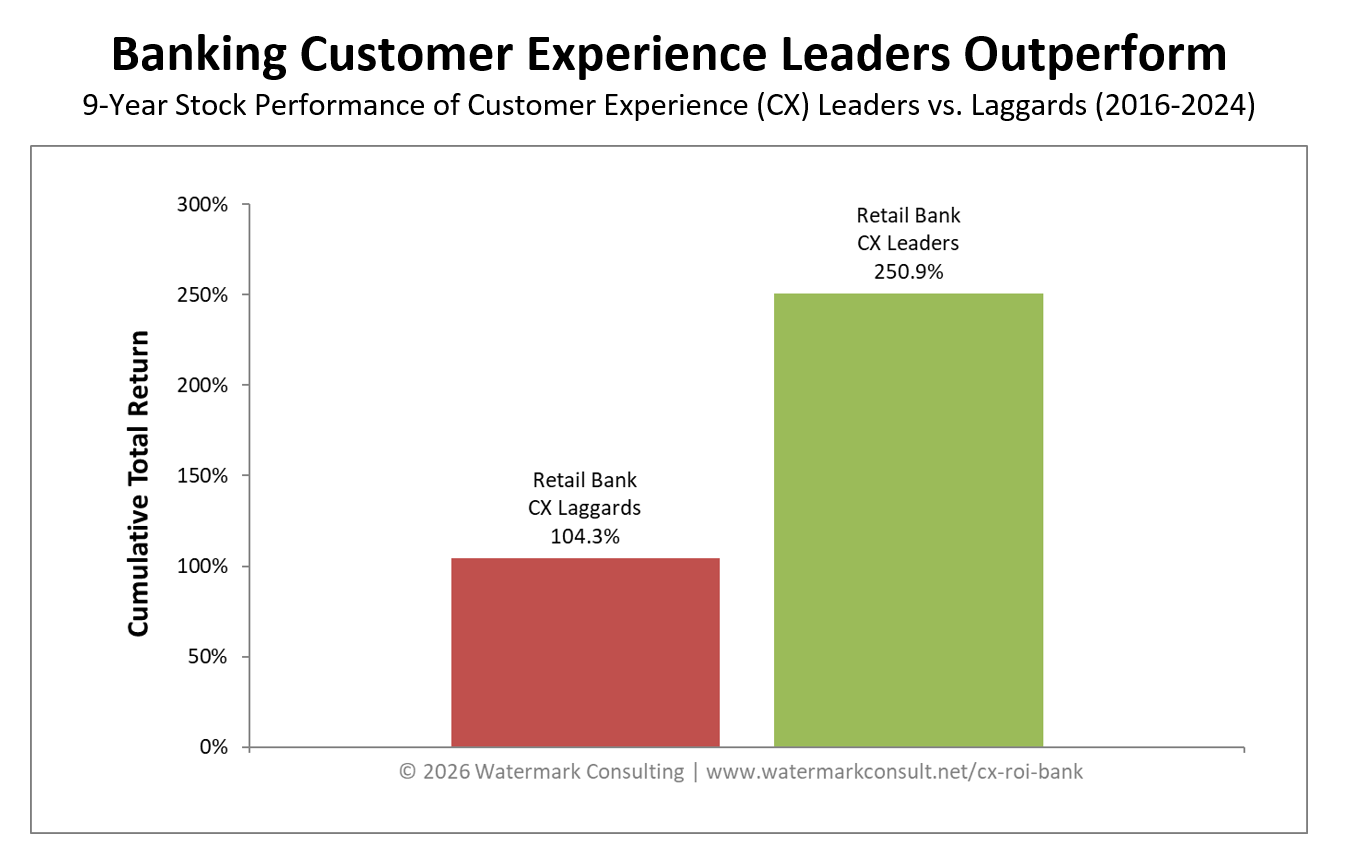

As the graphic below vividly illustrates, the results of our Banking Customer Experience ROI Study are quite compelling.

Banking CX ROI Study Results

Our analysis incorporates 9 years of customer experience rankings for national banks (defined by J.D. Power as those with at least 200 branches and more than $250 billion in domestic deposits). The graph below shows the cumulative total return across that period for the Banking Customer Experience Leaders and Laggards.

-

Banking Customer Experience Leaders far outperformed the Laggards, and the size of the performance differential (nearly 150 points) was striking.

-

The Leaders generated a total cumulative return that was 2.4 times greater than that of the Laggards.

Behind The Numbers

It’s worth underscoring that this analysis reflects nearly a decade of performance results. Over that period, the fortunes of Banking Customer Experience Leaders and Laggards have diverged in a dramatic and revealing way. What’s driving the disparity in performance across these two groups?

While there are obviously many factors that influence a company’s stock price, the results of this study indicate that, over the long-term, a great customer experience helps build banks’ business value, while a poor customer experience erodes it. That’s an important takeaway, for public and private entities alike.

But what exactly is creating that enhanced value? Answering that question requires understanding the economic calculus behind great customer experiences. When a company consistently delivers an impressive experience to customers, it triggers behaviors that influence business financials in two important ways:

- A great CX helps grow revenues. When most people think about the economic benefit from a great customer experience, this is where their heads go. And that’s entirely appropriate, because revenue growth is indeed one clear advantage of CX excellence. Why? Happy, loyal customers have better retention, they’re less price-sensitive and they’re more willing to entertain offers for other products and services – all helping to raise revenue. Plus, because they love you so much, they spread positive word-of-mouth and refer new customers to you – lifting revenue even higher.

- A great CX helps control (if not reduce) expenses. This is the part of the customer experience economic equation that many businesses fail to appreciate. (It’s also why using revenue growth, alone, to demonstrate customer experience ROI is misguided.) When you have happy, loyal customers, it has a very favorable influence on operating expenses. For example, due to all the customer referrals you’re getting, you can spend less on new business acquisition – which reduces expenses. In addition, happy customers tend to complain less, putting reduced stress on your operating infrastructure (e.g., lower call and chat volumes), thereby also helping to keep expenses in check.

Higher revenues and a more competitive cost structure translate into superior profitability, and that’s what helps fuel exceptional shareholder returns for the CX Leaders.

Of course, those economic forces cut both ways. In contrast to the CX Leaders, the CX Laggards struggle to raise revenue (e.g., poor retention, high price-sensitivity, limited cross-purchasing, negative word-of-mouth) and they’re burdened with higher expenses (e.g., to acquire new customers, and to deal with the existing unhappy ones). This weighs on their long-term profitability and makes them less valuable in the eyes of the market.

Learn From The Leaders

How do Customer Experience Leading firms create such positive, loyalty-enhancing impressions on the people they serve? It doesn’t happen by accident. They’re all essentially employing the same strategic approach to achieve that outcome — and it’s an approach that Watermark has documented through its “12 Principles” (a CX design framework that is more fully described in Watermark Founder Jon Picoult’s book From Impressed To Obsessed).

In addition to those CX design techniques, the CX Leaders also embrace a few fundamental, shared philosophies that help guide their efforts:

1. They aim for more than customer satisfaction.

Satisfied customers defect all the time. And customers who are merely satisfied are far less likely to drive business growth through referrals, repeat purchases and reduced price sensitivity. Maximizing the return on CX investments requires more than just satisfying customers, it requires impressing them.

2. They leave nothing to chance.

The Leading companies have a keen appreciation for the wide array of live, print, and digital touchpoints that comprise their customer experience. They design each of these touchpoints very intentionally, carefully choreographing the interaction to create an experience that consistently nails the basics and also delivers pleasant surprises.

3. They shape memories, not just experiences.

How people remember the customer experience is arguably more important than the experience itself, as it’s those memories that ultimately drive repurchase and referral behavior. The Leading companies recognize this, and they use cognitive science to engineer experiences that people both enjoy in the moment and also remember fondly in the future.

4. They capitalize on the power of emotion.

People’s affinity toward a business is ultimately shaped by how they feel after interacting with the company, its representatives, and/or its products. CX-leading firms recognize this, and so they engineer experiences that don’t just focus on customers’ rational requirements, but also address their emotional needs.

5. They focus on both the customer and the employee experience.

Happy, engaged employees help create happy, loyal customers (who, in turn, help create more happy, engaged employees). The value of this virtuous cycle cannot be overstated, and it’s why the most successful companies address both sides of this equation – obsessing not just over their customers, but also over the employees who serve them.

Implications For Banks

The results of this study suggest there is competitive advantage to be gained in the banking industry by differentiating along the customer experience axis.

However, achieving that competitive differentiation requires that banks look at their business through a different lens, and embrace some unconventional operating principles – some examples of which we present below:

♦ Retention is not a good proxy for loyalty.

Banks often rely on account or deposit retention to gauge the quality of their customer experience. While retention is a valuable metric, it can be a misleading indicator of customer perception (after all, a retained customer may not necessarily be a loyal one).

As a result, many firms tend to overrate the quality of their customer experience, and would benefit by complementing their internal performance gauges (e.g., customer retention, deposit growth) with more externally and behaviorally-focused measures (e.g., customer referral frequency, Voice-of-the-Customer feedback surveys, qualitative customer research).

♦ Disclosure does not equal transparency.

The banking industry often points to its disclosure practices as evidence of its trustworthiness (i.e., “we’re not hiding anything from our customers, it’s all spelled out in our disclosures!”).

What the industry neglects to realize is that the manner by which information is disclosed is as consequential as the information itself. Deposit agreements and other types of disclosures are typically dense, difficult-to-read documents that leave the average consumer more confused than informed.

To earn customer trust, banks must strive for true transparency. That means eliminating the small print, skipping the legalese, and communicating with customers in clear, simple terms they can easily understand.

♦ Emotions are as critical as earnings.

Banks that focus primarily on interest rates and deposit earnings are destined to deliver a mediocre customer experience (or something worse).

The best and most memorable customer experiences are those that strike an emotional chord in people – be it by accentuating positive feelings or mitigating negative ones. Many financial institutions don’t fully appreciate this. As a result, they miss opportunities to enhance the customer experience by, for example, celebrating customers’ financial milestones or addressing their sources of financial anxiety.

Banking customers might not remember the exact interest rate they’re earning at any given moment, but they’ll surely remember how that bank made them feel – confident or confused, assured or anxious, informed or ignorant. When it comes to building customer loyalty, it’s those emotional responses that make all the difference.

♦ The mundane things matter.

If banks obsess over any part of their customer experience, it’s often on the human interactions that occur within a branch. While those are indeed a very important touchpoint, their frequency has diminished as consumers increasingly use digital channels to manage their financial affairs.

This dynamic amplifies the impact of routine, recurring touchpoints (many of them print and digital-based). Banks often treat these interactions (electronic transfers, account statements, bill paying services, etc.) as mundane, administrative tasks – and it shows in the resulting experience. However, for many customers, these mundane touchpoints are the entire experience, which is why these routine interactions deserve close attention and careful choreography.

♦ Trust and advocacy are critical.

As previously noted, there are serious trust issues between consumers and financial institutions — and that is deeply problematic given the important role banks play in people’s lives.

When consumers see banks employing business practices that clearly favor the institution over the individual (such as debit resequencing to maximize overdraft fees, or asymmetric interest rate-setting strategies where banks are slow to raise crediting rates but quick to lower them) — it erodes trust and saps loyalty.

Conversely, when banks tangibly advocate for their customers (such as by communicating clearly and transparently, proactively advising when more relevant and/or suitable products are available, or simply demonstrating exceptional ownership and urgency during problem resolution) — those can be relationship-defining moments that forge long-term brand loyalty.

Conclusion

Risk management is a fundamental component of the banking business — from asset/liability matching, to loan underwriting, to fraud mitigation.

Ironically, though, many in this industry are failing to address a key risk that looms over their organizations: the risk of just satisfying customers in a marketplace where it’s easier than ever for people to find substitute products, coupled with an environment where consumers are increasingly distrustful of financial institutions.

However, there is a solution. The best way for banks to avoid this death spiral is by delivering an exceptional end-to-end customer experience – one that is devoid of common frustrations, one that inspires confidence, one that cultivates trust. And, as this study has demonstrated, that’s the kind of customer experience that is rewarded by both Main Street and Wall Street.

(Want more? Check out Watermark’s other Customer Experience ROI Studies here.)

Ready to Turn Your Organization into a CX Leader?

Watermark is a customer experience advisory firm that serves some of the world’s leading brands. We help companies impress their customers and inspire their employees, creating raving fans that drive business growth.

What’s your challenge?

- We need to make the case for CX at our company. Our executive education programs will help demonstrate the value of customer experience excellence to company leaders, and show them how time-tested CX design techniques could be applied to your business.

- We don’t really know what customers think of us. Our Consulting Services include quantitative and qualitative tools which help bring the voice of your customer to the forefront, revealing game-changing insights that will drive your business forward.

- We need to rally our employees around CX. Watermark founder Jon Picoult is an acclaimed keynote speaker. Invite Jon to your next all-employee meeting, sales conference or corporate event – he’ll inspire your team to deliver CX excellence, and show them exactly how to do it.

- We need to improve our CX, but we’re not sure where or how to start. Our Consulting Services, including Watermark’s proprietary “Customer Experience Reality Check” will evaluate your current CX and develop a detailed roadmap for turning it into a competitive differentiator.

Through our Customer Experience ROI Studies, we’ve uncovered the techniques that top companies use to turn everyday people into loyal brand advocates. Let us help you apply the same techniques to your business. Contact us to start the conversation.

Study Methodology

The Watermark Consulting Insurance Customer Experience ROI Study is based on the cumulative total stock return for equally weighted, annually readjusted model portfolios comprised of Auto & Home Insurance Customer Experience (CX) Leaders and Laggards.

For each year covered by the study, CX Leaders and CX Laggards were identified via J.D. Power and Associates’ annual U.S. National Banking Satisfaction Studies. The Leaders and Laggards were generally defined as the Top 3 and Bottom 3 publicly traded companies in these rankings (approximately representing the top and bottom thirds of the ratings).

Portfolio returns were based on the prior-year performance of the Leaders and Laggards, to ensure that the results were not influenced by the publication of the research studies themselves.