About the Insurance Customer Experience ROI Study

What’s a great customer experience really worth to an insurer?

What’s a great customer experience really worth to an insurer?

It’s a fair question in an industry that many would characterize as a commoditized business, where consumers often gravitate to the insurance companies that offer the lowest premium.

However, we suspected that there were other experiential attributes (beyond price) that helped shape consumers’ selection of an insurance carrier, as well as influence the word of mouth they spread to other potential buyers.

So, we set out to determine if there really was a Customer Experience ROI, even in the seemingly commoditized business of insurance. We sought to explore the impact of good and bad policyholder experiences, using the universal business “language” of shareholder value.

What we discovered should be of keen interest to insurance executives, as well as any business leader who questions the value of customer-centricity. That’s because, as it turns out, there’s a big reward for insurers that impress their customers, and a lot of risk for those that don’t.

Best regards,

Jon Picoult

Founder & Principal, Watermark Consulting

Author, From Impressed To Obsessed

(Follow me on LinkedIn and Instagram)

The Business Challenge

Insurance is a grudge purchase – and that’s one of the biggest challenges insurers face as they try to build customer engagement and loyalty around a product people don’t want to buy and hope they never have to use. To combat these headwinds, and shape consumer perceptions more favorably, the insurance industry spends tens of billions of dollars each year in advertising.

However, as these companies will eventually discover, you can’t advertise your way to a great customer experience. Ultimately, customers’ perceptions will be shaped by the end-to-end experience itself – from how they’re onboarded, to how their needs are assessed, to how rate changes are communicated, to how claims are handled, etc.

Nevertheless, many insurers cling to a product-centric, rather than customer-centric, view of the world. To put it bluntly, this is an industry that is far more enamored with acquiring new customers than it is with delighting the ones they already have.

For all the money they spend on advertising, insurers tend to hold the purse strings much tighter when it comes to investments in a better customer experience — viewing the benefits as soft and intangible, the payoff uncertain. As a result, they continue to subject customers to a whole host of aggravations and indignities: complex product offerings, complicated purchase processes, unexplained rate increases, confusing policy documents and disclosures, interminable waits for customer service, infuriatingly unhelpful AI chatbots, and an overall business model that breeds mistrust (the less insurers pay in claims, the more they profit).

There are exceptions, however. A handful of insurers are very deliberate in how they shape the end-to-end, prospect-to-policyowner-to-claimant experience. And, as you’ll see in a moment, that strategy is rewarded by consumers and investors alike.

First, though, an explanation of the thought process behind the Insurance Customer Experience ROI Study:

Our objective with this analysis was to help industry leaders understand the overarching influence of a great customer experience (as well as a poor one). To accomplish that, we sought to elevate the dialogue. That meant getting the industry to focus, at least for a moment, not on the cost/benefit of specific customer experience initiatives, but rather, on the macro impact of an effective customer experience strategy.

We accomplished this by studying the cumulative total stock returns for two model portfolios – comprised of the Top 5 (“Leaders”) and Bottom 5 (“Laggards”) publicly traded companies in J.D. Power and Associates’ annual Insurance Satisfaction Studies. (A full description of the study’s methodology is available at the bottom of this article, and we’ve also compiled a list of frequently asked questions about the analysis.)

As the graphs that follow vividly illustrate, the results of our latest Insurance Customer Experience ROI Study continue to be quite compelling.

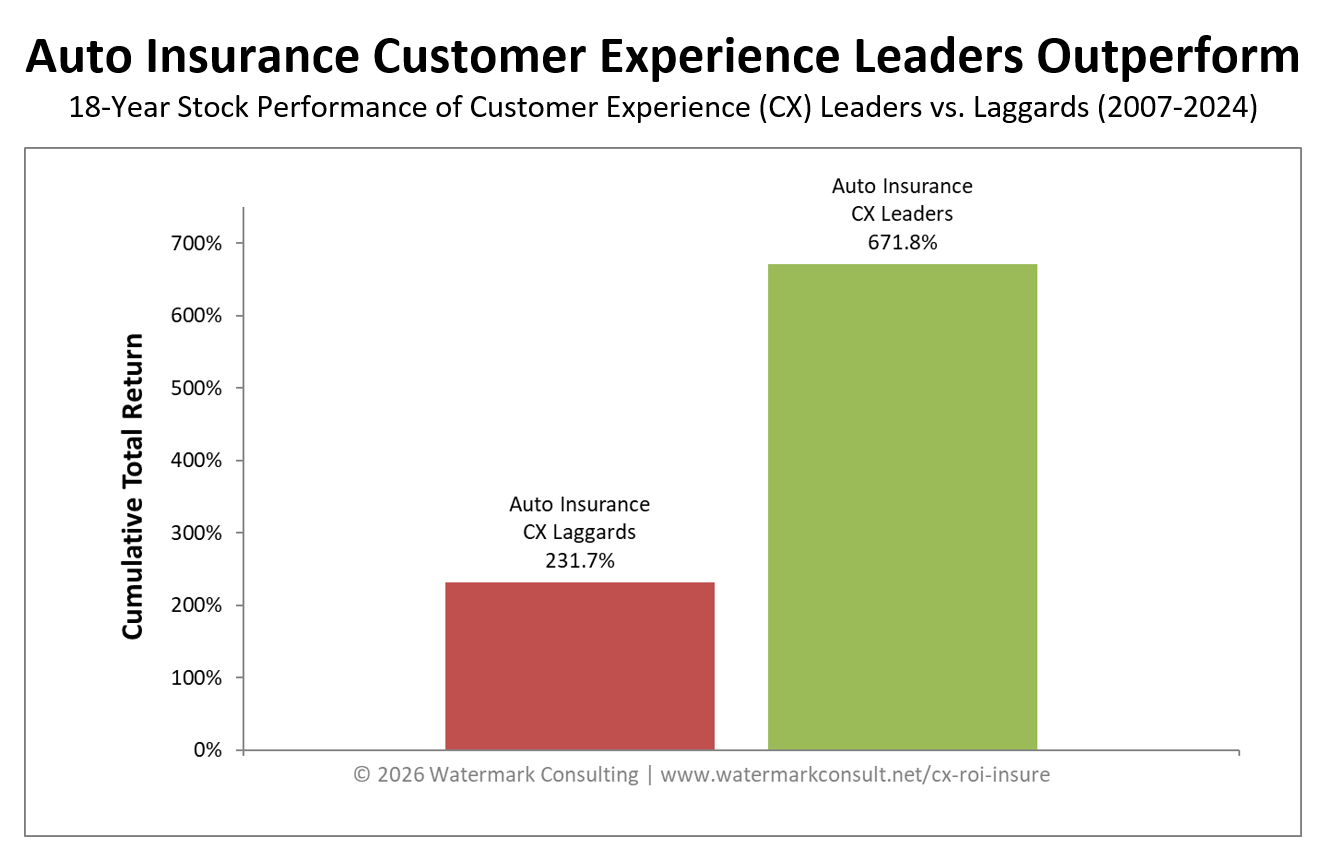

CX ROI Study Results — Auto Insurance

Our latest analysis incorporates 18 years of customer experience rankings for automobile insurance companies. The graph below shows the cumulative total return across that period for the Customer Experience Leaders and Laggards.

-

Auto Insurance Customer Experience Leaders far outperformed the Laggards, and the size of the performance differential (440 points) was striking.

-

Auto Insurance Customer Experience Leaders generated a total cumulative return that was 2.9 times greater than that of the Customer Experience Laggards.

-

The performance gap between the Auto Insurance CX Leaders & Laggards has more than doubled over the past five years.

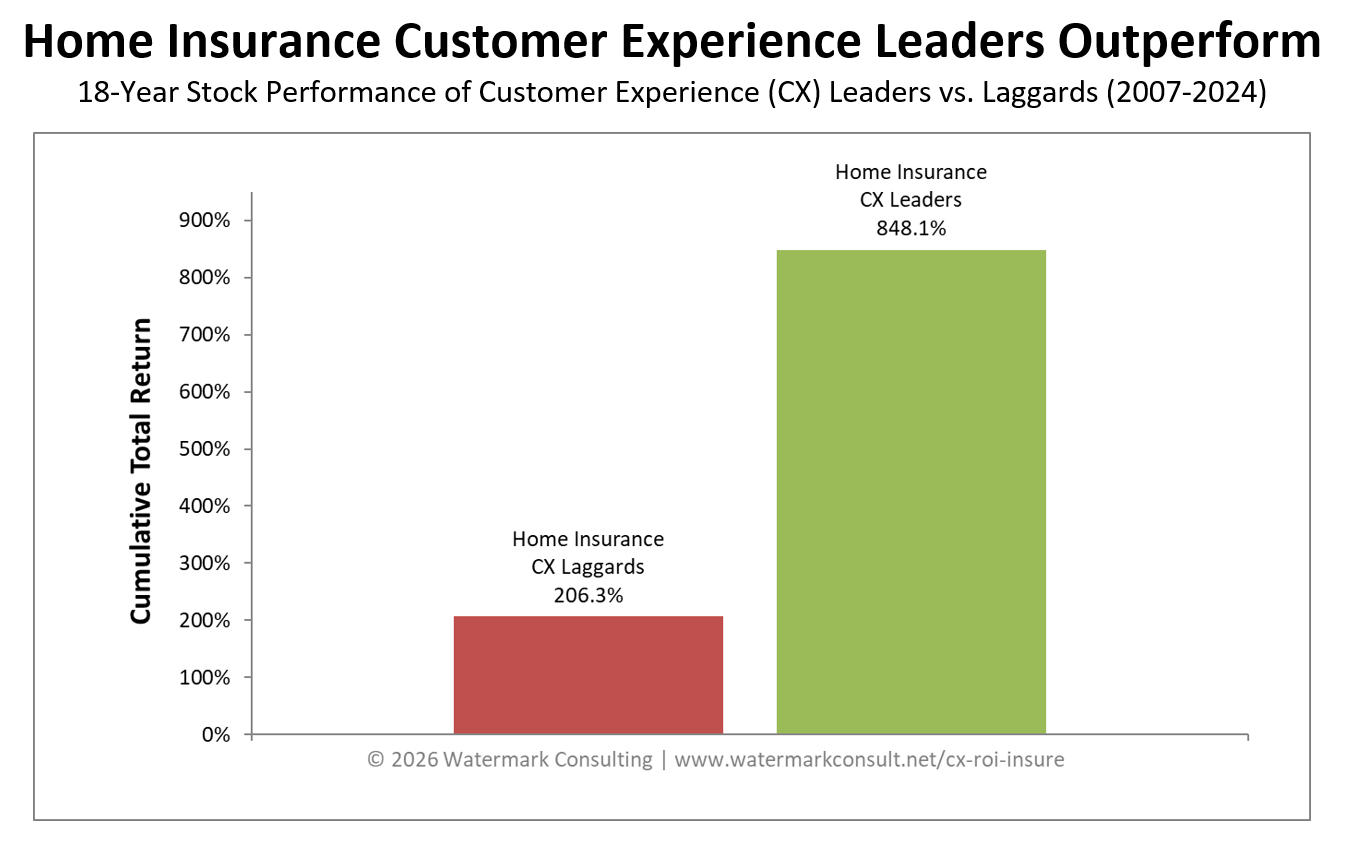

CX ROI Study Results — Home Insurance

Our latest analysis incorporates 18 years of customer experience rankings for homeowner’s insurance companies. The graph below shows the cumulative total return across that period for the Customer Experience Leaders and Laggards.

-

Home Insurance Customer Experience Leaders far outperformed the Laggards, and the size of the performance differential (over 640 points) was truly remarkable.

-

Home Insurance Customer Experience Leaders generated a total cumulative return that was a stunning 4.1 times greater than that of the Customer Experience Laggards.

-

The performance gap between the Home Insurance CX Leaders & Laggards has more than doubled over the past five years.

Behind The Numbers

It’s worth underscoring that this analysis reflects nearly two decades of performance results, spanning entire economic cycles, from expansions to recessions. Over that period, the fortunes of Insurance Customer Experience Leaders and Laggards have diverged in a dramatic and revealing way. What’s driving the disparity in performance across these two groups?

While there are obviously many factors that influence a company’s stock price, the results of this study indicate that, over the long-term, a great customer experience helps build insurers’ business value, while a poor customer experience erodes it. That’s an important takeaway, for public and private entities alike.

But what exactly is creating that enhanced value? Answering that question requires understanding the economic calculus behind great customer experiences. When a company consistently delivers an impressive experience to customers, it triggers behaviors that influence business financials in two important ways:

- A great CX helps grow revenues. When most people think about the economic benefit from a great customer experience, this is where their heads go. And that’s entirely appropriate, because revenue growth is indeed one clear advantage of CX excellence. Why? Happy, loyal customers have better retention, they’re less price-sensitive and they’re more willing to entertain offers for other products and services – all helping to raise revenue. Plus, because they love you so much, they spread positive word-of-mouth and refer new customers to you – lifting revenue even higher.

- A great CX helps control (if not reduce) expenses. This is the part of the customer experience economic equation that many businesses fail to appreciate. (It’s also why using revenue growth, alone, to demonstrate customer experience ROI is misguided.) When you have happy, loyal customers, it has a very favorable influence on operating expenses. For example, due to all the customer referrals you’re getting, you can spend less on new business acquisition – which reduces expenses. In addition, happy customers tend to complain less, putting reduced stress on your operating infrastructure (e.g., lower call and chat volumes), thereby also helping to keep expenses in check.

Higher revenues and a more competitive cost structure translate into superior profitability, and that’s what helps fuel exceptional shareholder returns for the CX Leaders.

Of course, those economic forces cut both ways. In contrast to the CX Leaders, the CX Laggards struggle to raise revenue (e.g., poor retention, high price-sensitivity, limited cross-purchasing, negative word-of-mouth) and they’re burdened with higher expenses (e.g., to acquire new customers, and to deal with the existing unhappy ones). This weighs on their long-term profitability and makes them less valuable in the eyes of the market.

Learn From The Leaders

How do Customer Experience Leading firms create such positive, loyalty-enhancing impressions on the people they serve? It doesn’t happen by accident. They’re all essentially employing the same strategic approach to achieve that outcome — and it’s an approach that Watermark has documented through its “12 Principles” (a CX design framework that is more fully described in Watermark Founder Jon Picoult’s book From Impressed To Obsessed).

In addition to those CX design techniques, the CX Leaders also embrace a few fundamental, shared philosophies that help guide their efforts:

1. They aim for more than customer satisfaction.

Satisfied customers defect all the time. And customers who are merely satisfied are far less likely to drive business growth through referrals, repeat purchases and reduced price sensitivity. Maximizing the return on CX investments requires more than just satisfying customers, it requires impressing them.

2. They leave nothing to chance.

The Leading companies have a keen appreciation for the wide array of live, print, and digital touchpoints that comprise their customer experience. They design each of these touchpoints very intentionally, carefully choreographing the interaction to create an experience that consistently nails the basics and also delivers pleasant surprises.

3. They shape memories, not just experiences.

How people remember the customer experience is arguably more important than the experience itself, as it’s those memories that ultimately drive repurchase and referral behavior. The Leading companies recognize this, and they use cognitive science to engineer experiences that people both enjoy in the moment and also remember fondly in the future.

4. They capitalize on the power of emotion.

People’s affinity toward a business is ultimately shaped by how they feel after interacting with the company, its representatives, and/or its products. CX-leading firms recognize this, and so they engineer experiences that don’t just focus on customers’ rational requirements, but also address their emotional needs.

5. They focus on both the customer and the employee experience.

Happy, engaged employees help create happy, loyal customers (who, in turn, help create more happy, engaged employees). The value of this virtuous cycle cannot be overstated, and it’s why the most successful companies address both sides of this equation – obsessing not just over their customers, but also over the employees who serve them.

Implications For Insurance Providers

Insurance providers tend to set the CX bar low for themselves, given the “grudge purchase” consumer mentality. With a starting point like that, how realistic is it for insurers to deliver anything but a mediocre customer experience?

Apparently, it is realistic to strive for something more, because the CX Leaders in this study are accomplishing precisely that, and gaining competitive advantage as a result. However, achieving that competitive differentiation requires that insurers look at their business through a different lens, and embrace some unconventional operating principles – some examples of which we present below:

♦ Retention is not a good proxy for loyalty.

Insurance providers often rely on policyholder retention to gauge the quality of their customer experience. While retention is a valuable metric, it can be a misleading indicator of customer perception (after all, a retained policyowner may not necessarily be a loyal one). As a result, many insurers tend to overrate the quality of their customer experience, and would benefit by complementing their internal performance gauges (e.g., policyholder retention, premium growth) with more externally and behaviorally-focused measures (e.g., customer referral frequency, Voice-of-the-Customer feedback surveys, qualitative policyholder research).

♦ Insurance can be more than a grudge purchase.

Some industry insiders question the viability of a customer-focused business strategy in insurance, given it’s an intangible product that people must buy, never knowing if they’ll get any benefit in return. Successful providers overcome this perception by engaging customers with value-added services that transcend traditional insurance coverage (such as discounted smart home devices, risk mitigation consultations, and automobile purchasing services).

♦ It’s essential to focus on more than just claims.

As the ultimate moment-of-truth in insurance, it’s critical that the claims customer experience be exceptional. However, the vast majority of insureds won’t experience a claim in any given year (unless the carrier is absolutely awful at underwriting — in which case they’ll have bigger problems to address!). For this reason, insurers’ experience improvement programs must go beyond claims – targeting other, more common customer touchpoints.

♦ The mundane things matter.

Insurance is a low interaction business, which amplifies the impact of routine, recurring transactions on customer perceptions. Firms often treat these interactions (policy delivery, billing, renewal, etc.) as mundane, administrative tasks – and it shows in the resulting experience. However, for many insureds, these mundane touchpoints are the entire experience, which is why these routine interactions deserve close attention and careful choreography.

♦ Trust and advocacy are critical.

There is an inherent lack of trust between many insurers and insureds given the nature of the relationship between the parties (the less carriers pay in claims, the more money they make). With trust being a key driver in policyholder satisfaction, it’s important for insurers to tangibly demonstrate their advocacy for customers — by, for example, quickly paying claims, as well as proactively communicating with policyholders to advise of (and help them mitigate) impending premium increases. These types of tactics help counter consumers’ perceptions of misaligned interests.

Conclusion

One key accountability of insurance providers is to help their customers manage risk. Ironically, though, many in this industry are failing to address a key risk that looms over their business: the risk that they become marginalized in an environment where their products and services are viewed as a commodity.

However, there is a solution. The best way for insurance providers to avoid the death spiral of commoditization is by delivering an exceptional end-to-end customer experience – one that is devoid of common frustrations, one that inspires confidence, one that cultivates trust.

As this study has demonstrated, that’s the kind of customer experience that is rewarded by both Main Street and Wall Street.

(Want more? Check out Watermark’s other Customer Experience ROI Studies here.)

Ready to Turn Your Organization into a CX Leader?

Watermark is a customer experience advisory firm that serves some of the world’s leading brands. We help companies impress their customers and inspire their employees, creating raving fans that drive business growth.

What’s your challenge?

- We need to make the case for CX at our company. Our executive education programs will help demonstrate the value of customer experience excellence to company leaders, and show them how time-tested CX design techniques could be applied to your business.

- We don’t really know what customers think of us. Our Consulting Services include quantitative and qualitative tools which help bring the voice of your customer to the forefront, revealing game-changing insights that will drive your business forward.

- We need to rally our employees around CX. Watermark founder Jon Picoult is an acclaimed keynote speaker. Invite Jon to your next all-employee meeting, sales conference or corporate event – he’ll inspire your team to deliver CX excellence, and show them exactly how to do it.

- We need to improve our CX, but we’re not sure where or how to start. Our Consulting Services, including Watermark’s proprietary “Customer Experience Reality Check” will evaluate your current CX and develop a detailed roadmap for turning it into a competitive differentiator.

Through our Customer Experience ROI Studies, we’ve uncovered the techniques that top companies use to turn everyday people into loyal brand advocates. Let us help you apply the same techniques to your business. Contact us to start the conversation.

Study Methodology

The Watermark Consulting Insurance Customer Experience ROI Study is based on the cumulative total stock return for equally weighted, annually readjusted model portfolios comprised of Auto & Home Insurance Customer Experience (CX) Leaders and Laggards.

For each year covered by the study, CX Leaders and CX Laggards were identified via J.D. Power and Associates’ annual U.S. Auto Insurance and Home Insurance Studies. The Leaders and Laggards were generally defined as the Top 5 and Bottom 5 publicly traded companies in these rankings (approximately representing the top and bottom thirds of the ratings). Where necessary, national rankings were derived by averaging insurers’ regional satisfaction scores.

Portfolio returns were based on the prior-year performance of the Leaders and Laggards, to ensure that the results were not influenced by the publication of the research studies themselves.